Building Business Resilience Through Stress Testing

Picture this: You’ve spent a month preparing a full business plan with financial projections for the next year. You look at the results and think "This will be a great year!".

But what happens if you suddenly lost your biggest customer? What happens if your costs went up 15%? What happens if your key supplier cuts off trade terms?

You won’t know for certain and this is where stress testing comes in handy.

In this issue, you will learn:

- How stress testing makes your business resilient

- Relevant testing parameters vs. performance metrics

- Actionable takeaways

Stress testing builds business resiliency

Stress testing is a risk mitigation strategy that tests various hypothetical scenarios against your financial projections to assess how well your business can adapt to adverse conditions.

All business plans, to an extent, are based on assumptions. These assumptions are based on inputs that carry countless uncertainties. There are internal inputs provided by each department based on their set goals and targets, which you have control over. On the other hand, there are external inputs such as rising interest rates or variability in input costs, which are out of your control.

What stress testing does is it models out how changes in the variable(s) impact your financial statements. This gives you a clarity on the potential impacts to guide you through your with strategic decision making process.

There are 3 key aspects stress testing provides:

- It identifies vulnerabilities and weak points by pinpointing potential risks and assessing the impact of external factors

- It enables strategic planning and proactively responds to potential challenges

- It builds stakeholder and investor confidence by demonstrating risk management competency

Now that you understand the background, let’s dive into the fun.

Relevant Testing Parameters vs. Performance Metrics

To stress test, you must have a fully formula-linked financial model that is capable of adjusting variables that automatically filters through the model.

Once this is ready, we focus on the inputs and outputs.

- Inputs: These are the key risk factors or variables being tested. While there are endless inputs to consider, it must be specific to your business needs.

- Outputs: These are critical financial metrics about the company’s financial health. Such metrics are focused on the company’s profitability, cash flow, and covenants.

Let’s go through a series of examples to see how stress testing works.

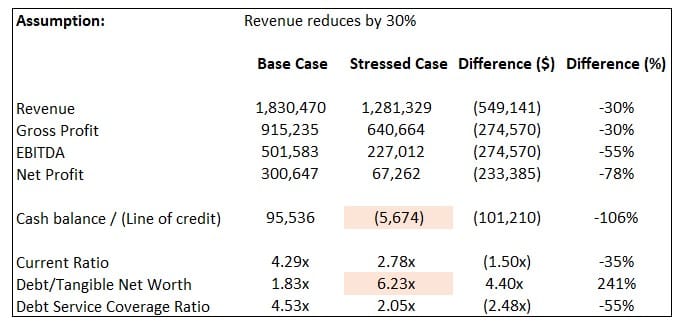

Example 1: Loss of revenue

Purpose: Test against the risk of loss of revenue.

Reason: There are many reasons for revenue loss. Risk factors impacting revenue include loss of top clients due to customer concentration risk , loss of market share from the competitive landscape, loss of sales staff (employee turnover), or a changes in consumer preferences.

Example:

Assessment:

Following a 30% revenue reduction, the initial assessment notes that the company remains profitable. However, the revenue reduction has translated to a 55% reduction in EBITDA and 78% reduction in net profit. While it's still positive and not the end of the world, the reduction is huge.

The company’s cash balances and covenants, however, tell a different story. The lower net profit has significantly reduced the company’s cash balances and tangible net worth. This means:

- The company will need to use their line of credit (if they have one) to offset the negative cash balance. Otherwise, cash injections will be required.

- The combination of higher debt and lower tangible net worth has elevated the company’s leverage position. The covenant for debt to tangible net worth covenant is typically set at 2.50x - 3.00x. The company way offside this threshold and will need to improve profitability or reduce debt (or both).

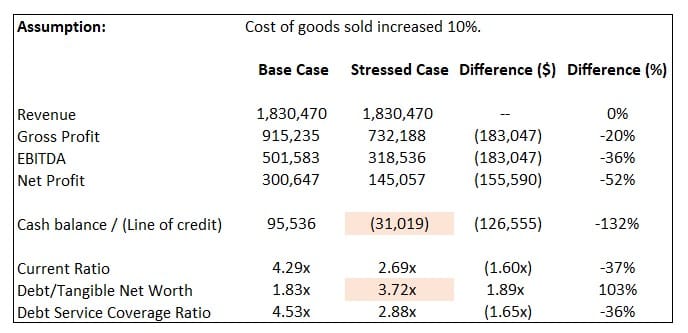

Example 2: Elevated input costs

Purpose: Test the impacts of rising input costs.

Reason: Input costs to the business can be a mix of internal and external factors. Internal factors include inefficient production processes, rising labour costs, and equipment breakdowns. External factors include rising material and transportation costs.

Example:

Assessment:

Similar to the impacts of the revenue reduction above, a reduction in gross profit margin of 10% has resulted in reduced profitability. Similarly, this has impacted the company’s cash position and debt to tangible net worth covenant.

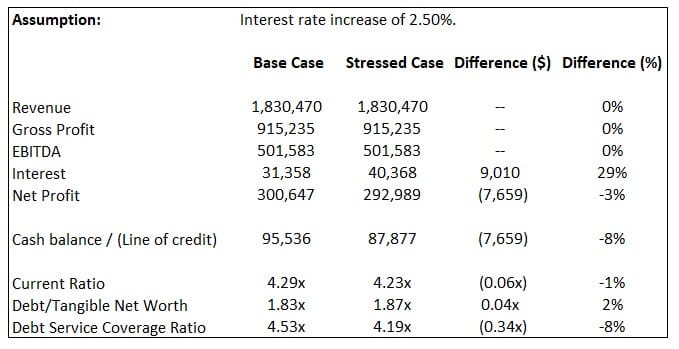

Example 3: Rising interest rate

Purpose: Test the impact of rising interest rates.

Reason: Interest rates are external factors based on central bank policies and economic environments. An upward swing in interest rates can significantly impact companies who are highly carry a lot of debt. This test assesses the company's ability to cover interest payments and debt servicing requirements.

Example:

Assessment:

Based on a 2.5% increase in interest rate, the company has sufficient operating income to withstand the interest rate hike. Keep in mind, the Fed increased interest rates from 0.25% to 5.25% from March 2022 onwards. A 5% swing in interest rate can break a company’s debt serviceability, especially for those with thinner profitability levels.

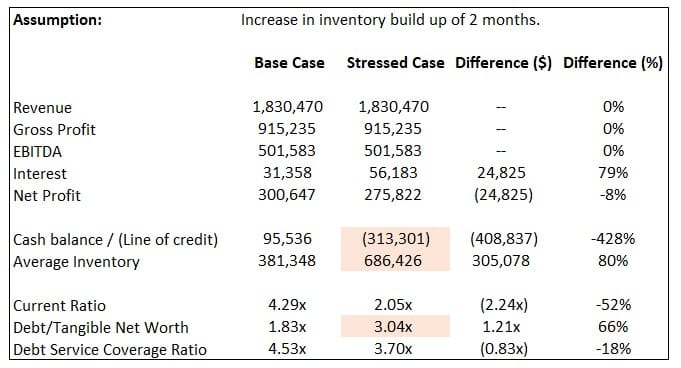

Example 4: Supply chain disruptions

Purpose: Test the impact of delays in material/inventory procurement.

Reason: When a company is reliant on key suppliers to provide essential materials for manufacturing or reselling, supply chain disruptions can put the company at a standstill. The company won't have enough products to sell. To prevent this, companies may opt to carry additional inventory to prevent supply chain disruptions. This test assesses the company’s ability to carry a longer cash conversion cycle.

Example:

Assessment:

In the wake of Covid-19, the world’s supply chain crumbled to the ground. Panic ensued and companies across the world opted to stock up supplies for as long as they can afford to. In this scenario, 2 extra months of inventory was modelled. Here are the impacts:

- Average inventory levels increased by $305k (80%).

- Building inventory depleted all of the company’s cash, dipping heavily into the line of credit for $313k.

- Higher line of credit utilization increased debt and added $25k in interest cost.

Altogether, the company breached its debt to tangible net worth covenant and could potentially be in excess of their line of credit. This means the company doesn't have the financial capacity to add 2 extra months of inventory to hedge against supply chain disruptions. Instead, the company can try modelling for 1 month of inventory.

There are endless stress testing variables to consider so picking the relevant factors will be important. Other testing variables include:

- Supplier relationships: Test for the impact on cash flow against shortened credit terms from suppliers.

- Market volatility: Test for impact on companies with exposure to multiple currencies.

- Commodity price swings: Test the impact on commodity prices against production costs.

- Employee turnover: Test the impacts on high employee turnover to assess reduction in productivity and higher training costs.

- Technology failures: Test the financial impacts of failed technology systems and cyberattacks.

Actionable Takeaways:

There’s a lot to unpack from the examples above. Here are some actionable steps to take now:

- Financial model: You must have a financial model capable of adjusting inputs to automatically apply changes throughout the financial projection. The model needs to include all relevant variables and historical data for accurate projections.

- Determine the key risks: Determining the key risk specific to the company’s industry, market, and internal operations.

- Conduct stress testing: Tweak the individual variables within the financial model to assess its impact on the financial metrics. Adjusting a combination of variables is possible; it will add complexity to your decision-making process.

- Establish contingency plans: Develop specific contingency plans to counter the identified risks.

- Update regularly: Stress testing is not an annual exercise. The financial model should be updated regularly. Business decisions are made throughout the year and is best most informed when the most recent financial data and assumptions are used.

To summarize, you now understand the power of stress testing analysis and its role in enhancing the financial resiliency of your company. By evaluating various risk factors and simulating unforeseen events, stress testing allows you to identify potential vulnerabilities and weak points in your business. Using this knowledge will help you make informed strategic decisions and proactively respond to potential challenges.

Let’s get testing!

That's it for this week. Thank you for reading Financing Journey. See you next Saturday.

If you’ve enjoyed this issue, don’t forget to subscribe here for weekly tips delivered straight to your inbox.

If you think this would be helpful to anyone you know, please share this newsletter and connect with me on X and LinkedIn for daily financing tips.

Have a topic you'd like me to cover? Email me at hello@lawrencefan.com.