Case study: Line of credit for a growing distributor

This case study will show you how banks determine the sizing and terms of the credit facility (and the nuances that go with it). With the financial markets being as volatile as they are today, having access to bank financing can make the difference between a business that struggles and one that thrives.

*** Please note this case study is based on a hypothetical specialty foods distributor. Actual financing terms will vary based on individual business circumstances, bank policies, and market conditions. ***

Gourmet Distributors, Inc.

To set the stage, Gourmet Distributors is a specialty food distributor with ~$20M in revenue and a strong balance sheet. Business is growing and the company is looking for additional dry powder (i.e. capital) to invest into their business.

Why Gourmet Distributors Needs Bank Financing

Like many distribution businesses, Gourmet Distributors faces several cash flow challenges:

- Timing Gaps: The food industry has extremely short credit terms so they pay suppliers for inventory upfront but may wait 30-45 days to receive payment from their restaurant and retail customers.

- Seasonal Inventory Needs: During peak holiday seasons, they need to stock up on specialty food products months in advance to meet demand.

- Growth Opportunities: To expand their product line or enter new markets, they need ready access to capital without depleting cash reserves.

- Equipment Updates: Delivery trucks and warehouse equipment need regular updating to maintain efficiency.

Without proper financing, the company might miss growth opportunities, struggle with cash flow during seasonal peaks, or be forced to decline large orders from new customers due to inventory limitations.

How Bank Financing Can Help the Business Grow

The right bank financing solution serves as a powerful growth tool by:

- Bridging Cash Flow Gaps: Financing inventory purchases while waiting for customer payments keeps operations smooth.

- Enabling Bulk Purchasing: The ability to buy in larger quantities can secure better pricing from suppliers.

- Supporting Expansion: Having capital available allows for pursuing new customers, territories, or product lines.

- Preserving Cash Reserves: Using bank financing for predictable needs keeps cash available for unexpected opportunities or challenges.

- Improving Supplier Relationships: Paying suppliers promptly can lead to preferential treatment and better terms.

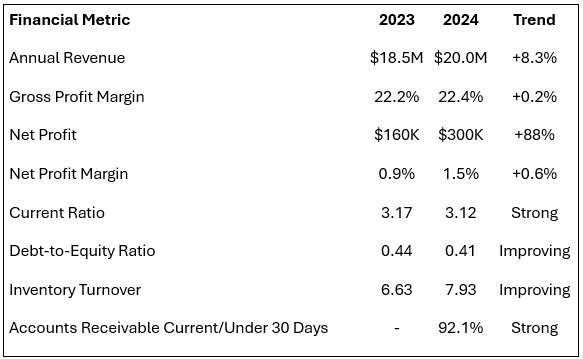

Financial Snapshot of Gourmet Distributors

Before diving into the financing structure, let's look at the key financial metrics that make this company a good candidate for bank financing:

These numbers tell the story of a growing, financially stable company with improving profitability and strong asset management. The business has low leverage (debt) and maintains healthy liquidity. This financial profile makes it an attractive candidate for bank financing and directly influences the structure I've recommended below.

A full set of financial statements is attached here for reference.

Financial info - Gourmet Distributors.xlsx

The Financing Structure

For Gourmet Distributors, I've developed a financing package tailored to their distribution business model:

Operating Line of Credit: $2,000,000

- Purpose: Day-to-day working capital, inventory purchases, and managing seasonal peaks

- Structure: Demand facility (can be called by the bank, if necessary)

- Security: First position on all assets of the company

- Interest Rate: Prime + 0.75%

- Set-up Fee: 0.50% of the facility amount

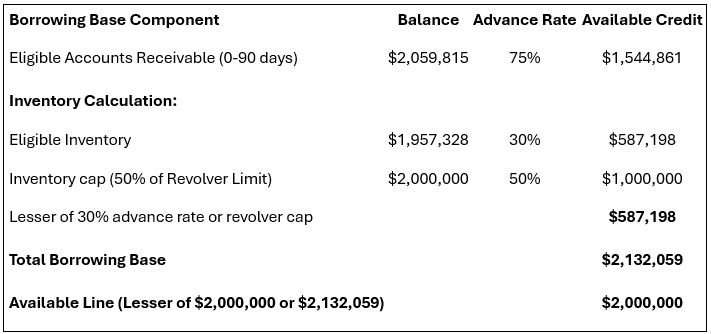

The Borrowing Base

The availability of funds within the $2 million line of credit will be based on the company’s borrowing base, which is calculated using the liquid assets of the company, namely their accounts receivable and inventory. As these fluctuate monthly, the amount of credit available to Gourmet Distributors will change. Here’s the formula for Gourmet Distributor's borrowing base:

The maximum available at any time is the lesser of $2,000,000 or:

- 75% of eligible accounts receivable (invoices less than 90 days old)

- PLUS the lesser of:

- 30% of eligible inventory value, OR

- 50% of the $2,000,000 revolver limit ($1,000,000)

- LESS priority payables.

Here’s a sample calculation based on their year end balance sheet figures.

As shown above, this structure provides $2 million in borrowing capacity based on their current financial position as of December 31, 2024.

Understanding the Margin Rates on AR and Inventory

Banks don't lend the full value of receivables and inventory because they need a safety margin. Here's why:

Accounts Receivable - 75% Advance Rate:

The 75% advance rate on accounts receivable reflects the bank's assessment of what they could realistically recover if the company faced financial distress, and the bank needed to collect these receivables directly. This rate isn't arbitrary—it's based on industry experience showing that when a lender must step in to collect receivables in a liquidation scenario, they recover about 75 cents on the dollar (often less). The 25% discount accounts for the challenges of collection in a distressed scenario, including the time value of money during the extended collection period and the likelihood that some customers might delay or resist payment when dealing with a lender rather than their regular supplier.

Inventory - 30% Advance Rate:

The 30% advance rate on inventory represents an even more conservative approach (typical rate is 50%) because Gourmet Distributor’s inventory poses greater risks as collateral. If a bank had to liquidate food inventory, they would face significant challenges: specialized food products often sell for pennies on the dollar in forced liquidation; perishable items have limited shelf life and could lose value rapidly; storage and handling during liquidation create additional costs; and finding buyers for bulk specialty food items in a rush can be difficult. The 30% rate gives the bank confidence that even in a worst-case scenario, they can recover their loan value from the collateral.

These conservative advance rates protect both the bank and the business by ensuring the loan remains fully covered by realizable assets.

Key Risks and Mitigants

Every financing arrangement involves risks that the bank will be concerned about. As a business owner seeking financing, you need to understand these risks from the bank's perspective and have plans to address them. Here are a few concerns banks will have about financing a specialty food distributor, and how you can proactively address them:

Risks:

- Thin Profit Margins: The specialty food distribution industry typically operates on narrow margins (1.5% net profit for Gourmet Distributors) as profits are typically generated through significant sales volume. Banks worry that small market shifts could quickly erase profits.

- Inventory Obsolescence: Food products can expire or lose marketability, potentially leaving the bank with collateral that's worth much less than expected.

- Customer Concentration: Reliance on a few large customers can create vulnerability if any of them were to leave or face financial difficulties.

- Seasonal Fluctuations: Cash needs can vary significantly throughout the year, creating potential stress points in the business cycle.

Mitigants (How to Address the Bank's Concerns):

- Strong Track Record: Demonstrate consistent profitability and preferably improving performance (like Gourmet Distributors' profit increase from 0.9% to 1.5%).

- Healthy Balance Sheet: Maintain reasonable debt levels—Gourmet Distributors' debt-to-equity ratio of only 0.41 is very attractive to lenders. This shows that the owners have a lot of skin in the game through invested capital and retained earnings.

- Good Inventory Management: Show efficient inventory practices through metrics like turnover ratio improvements (from 6.6x to 7.9x in this case).

- Quality Receivables: Maintain strong collections practices, with the majority of accounts receivable current or only slightly past due (92% under 30 days for Gourmet Distributors).

- Diversified Customer Base: Document that no single customer represents more than 15-20% of your business.

Understanding these concerns and proactively addressing them in your financing proposal will significantly increase your chances of approval. Banks need to see that you understand your risks and have plans to manage them effectively.

Financial Covenants

Here comes the dreaded term “Financial Covenants”. The term has a bad rep but it really isn’t bad at all.

Financial covenants should be seen as important for both the bank and the borrower. For the bank, they provide early warning signals if the business is heading toward financial difficulty. For the borrower, they establish clear financial parameters to maintain good standing with the lender. Think of covenants as guardrails that help keep the relationship on track.

For Gourmet Distributors, I've recommended the following covenants:

- Current Ratio: Minimum 1.25x

- The company must have at least $1.25 in short-term assets for every $1 of short-term liabilities.

- Why it matters: This ensures the company maintains adequate liquidity to meet short-term obligations.

- Debt Service Coverage Ratio: Minimum 1.25x

- For every dollar of debt payments due, the company must generate at least $1.25 in available cash flow.

- Why it matters: This ensures the company generates enough cash to comfortably make its debt payments (principal AND interest).

- Leverage Ratio (Debt/EBITDA): Maximum 2.5x

- Total debt cannot exceed 2.5 times the company's annual earnings (before interest, taxes, depreciation, and amortization).

- Why it matters: This prevents the company from taking on excessive debt relative to its earnings capacity.

- Side note – Banks may opt for a Debt/Tangible Net Worth covenant but I have purposely structured this deal based on EBITDA instead. Gourmet Distributors has significant net worth ($5.7M), which would make this covenant inconsequential if it was ever tested against debt (max ~$2.6M).

These covenants are set at levels that provide the bank with early warning signs of potential problems while giving your business reasonable operating flexibility. By monitoring these metrics regularly (quarterly), you can avoid covenant breaches and maintain a strong relationship with your lender.

What to Prepare When Requesting Bank Financing

Here’s the fun part. Before you approach your banker to seek for financing, there are a handful of items you’ll need to prepare. Having these items ready will show professionalism and readiness to have a serious engagement for financing. Here’s what you’ll need.

Financial Information:

- 3 Years of Financial Statements: Preferably audited or reviewed by an accountant

- Current Year-to-Date Financials: Showing recent performance

- Accounts Receivable Aging Report: Breaking down receivables by age (0-30 days, 31-60 days, 60-90 days, and 90+ days)

- Inventory Listing: Detailed breakdown by product category and age

- Financial Projections: Showing expected performance for next 12-24 months

Business Information:

- Company History: Brief overview of the company's development

- Business Plan or Overview: Explaining the business model and growth strategy

- Customer Information: List of major customers and their percentage of sales

- Supplier Details: Major suppliers and payment terms

- Management Résumés: Background of key executives

Specific to Distribution Businesses:

- Seasonality Analysis: Showing historical patterns of peak inventory and sales periods

- Inventory Management Systems: Details on how inventory is tracked and managed

- Customer Contracts: Any long-term supply agreements

- Distribution Agreements: Exclusive distribution rights or territories

Conclusion

Bank financing, when properly structured, can be extremely useful for business growth. Gourmet Distributors' $2M line of credit provides the flexibility needed to manage cash flow gaps, take advantage of growth opportunities, and satisfy seasonal demands.

The key to getting bank financing is understanding what lenders look for: strong cash flow, quality collateral, seasoned management, and transparent financial reporting.

It also pays to know what banks think about the value of your assets so you can provided justified counters to maximize your lending value.

Remember that banks want to say "yes" to good loans – they make money by lending to successful businesses. The more you can demonstrate your creditworthiness, the better your chances of securing favorable financing terms.

If you found this case study helpful for understanding business financing options (or if you have any questions), I'd love to hear from you!

Feel free to drop me an email at hello@lawrencefan.com.

I'm always happy to chat about financing solutions that can help your business grow.

Cheers!

Lawrence