How to Choose Between a Fixed or Variable Interest Rate

Interest rates are always a hot topic of discussion.

Everyone from economists, to politicians, to your kids primary school teacher will have their view of interest rate trends. This is only normal, especially when the decision in choosing the right interest rate could result in overpaying or saving on your loan for years to come.

Should you fix it? Or leave it floating?

Here’s the answer: It depends.

Everyone wants to pay the least amount of interest over the life of the loan. But this shouldn't be the only deciding factor. There are many other factors that should be considered for your final decision so...

In this issue, you will learn:

- The difference between fixed and variable interest rates.

- The different variables to consider when choosing an interest rate option.

- How to decide which option works best for your company.

Here we go.

Fixed vs. Variable Rates

With a fixed-rate loan, the interest rate and size of payment will be the same each month throughout the term of the loan. A fixed interest rate means the rate remains unchanged over the selected term. In some instances, the fixed rate is considered to be the all-in rate. Regardless of market or economic activity, after you've locked in the fixed rate, it will not change.

With a variable-rate loan, the interest rate will change based on the financial index being referenced. Changes in the index are based on the overall health of the economy (i.e. inflation, unemployment, and etc.). The most common variable interest rate prices loans using Prime +/- a specified amount known as a spread. For example, if Prime was 7.20% and the loan was priced at Prime + 1.00%, the all in rate is 8.20%.

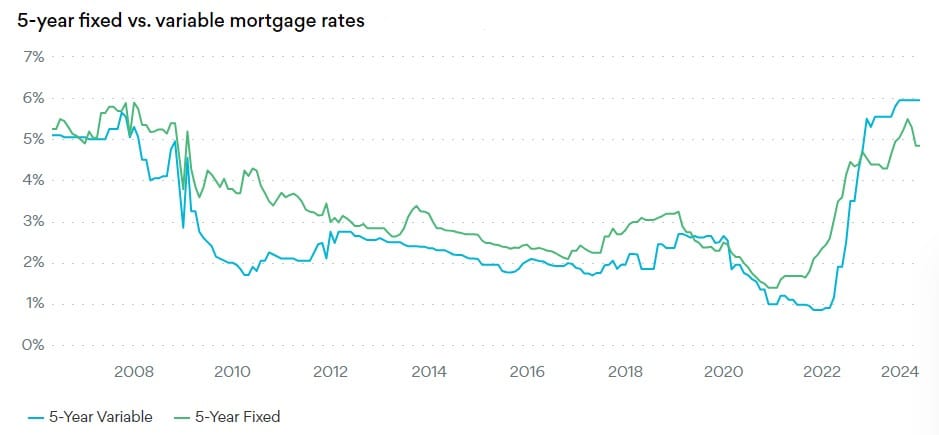

Historically, fixed rates have been higher than variable rates at any given point in time. This is because banks apply a premium on fixed rates to offset the basis risk of rising market interest rates, which reduces the market value of the corresponding loan.

In contrast, for variable rates, the borrower is the one who carries the potential risk of rising interest rates. When the bank carries less risk, pricing is reduced.

To make the point clear, look at the following graph highlighting the historical trend of fixed vs. floating rates.

In the past 12 months, fixed rates have been lower than variable rates as a result of an inverted yield curve. Without overcomplicating this topic, at the time of this writing, the market has priced in significant rate cuts for the next 3-5 years, which has parred down the overall fixed rate market.

Let's move into the key considerations to arrive at a decision.

The Different Variables to Consider

- Interest Rate Trends

The goal here is to understand the market outlook on the interest rate environment. This information is provided by central banks (i.e. the Fed or Bank of Canada) based on their view on the economy.

When interest rates are low, the general consensus is that rates will increase over time. By locking in a fixed rate, you will be protected from rate increases in the future.

Conversely, when interest rates are high, the outlook generally calls for rate cuts in the future. In this scenario, it may be beneficial to choose a floating rate to take advantage of potential rate cuts.

Side note, remember that historical trends aren't necessarily indicative of future performance so weigh your outlook judiciously.

- Type of Loan

Depending on the type of loan you have, the interest rate option may vary.

When the loan is a line of credit, a variable rates are typically used. This allows for maximum flexibility since the loan balance fluctuates over time.

For term loans, the interest rate can be either fixed or variable.

- Amortization Period

If the loan has a long horizon remaining (15+ years), it will make sense to opt for a variable rate. As illustrated above, variable rates have generally been lower than fixed rates.

For shorter tenor loans (5 years or less), it may be beneficial to fix the rate to avoid any short term rate volatility.

- Growth Prospects

If the company is going through a growth phase and is projected to have excess cash flow, it may be a good idea to choose a variable rate. By using the excess cash flow generated, the company can benefit with an option to make lump-sum principal payments up to a specific amount without penalty, which significantly reduces interest expenses over time. Also, the company has the ability to dampen the impact of higher interest expenses with increased probability.

- Stability of financial performance

If the company isn't financially stable, banks will assign a higher risk rating to the company and will offset this risk by increasing the spread on the loan. From the company's perspective, it can protect its exposure by securing an all-in fixed rate. This provides certainty of interest expenses so banks cannot simply raise the spread on the loan.

If the company has a steady track record of profitability, the probability of the bank raising the loan spread is low. Opting for a variable rate will make sense in this instance.

- Ease of Financial Planning

A financial plan always comes with a laundry list of assumptions. By fixing the interest rate, this takes away one key assumption while locking in the interest cost over the term of the loan. A predictable interest cost makes it easier for you to determine your margins.

This is especially helpful when your business is project based; working backwards using a fixed interest rate will help determine the contract price leading towards a greater probability of profitability.

When budgeting with a variable rate, companies typically assumes the lowest possible Prime rate throughout the term of the loan. Lenders will then sensitize this assumption based on their own perspective of the interest rate trends, which may impact their decision to lend.

- Company Size

Larger companies tend to use variable interest rates because their business are mature, stable, and have more cushion to withstand potential interest rate hikes. This means the large companies will feel less pain from rate hikes as opposed to smaller companies. This makes variable rates attractive since they have been historically cheaper to use.

Larger companies with larger loans have access to other types of interest options (i.e. SOFR or CORRA loans), which are generally less expensive than traditional prime based loans.

- Risk Appetite

Risk appetite is one of the most important considerations to make. Ultimately, it is based on the comfort level of the decision maker.

Some borrowers opt for a fixed rates because they want to have peace of mind and don't mind paying more for this luxury.

Other borrowers are comfortable riding the variable wave because they have a higher risk tolerance and don't mind floating, if the option ultimately saves money.

How to Decide Which Option Works Best?

With so many factors to consider, it's time to decide which option works best for you. Everyone's situation is unique with different priorities.

The best course of action is to begin by assessing your company's cash flow, financial flexibility, and the need for security.

Next, pair up your assessment to the key considerations above to see which interest rate option scores the most points.

Once you have come up with the tally, ask yourself if you can choose the option and forget about it for the rest of the term. If you can, you're set.

If not, what is holding you back from this decision? The answer will always bring out your #1 priority.

Remember, as a business owner, your ultimate priority is to operate and grow the business. You are not here to speculate interest rates. Choose the interest rate option that makes the most sense for you and your company.

And here's the best part of it all. No matter what decision you make, you won’t regret it. Just know that the decision that you made was the best possible option based on your circumstances at the time the decision was made.

That's it for this week. Thank you for reading Financing Journey. See you next Saturday.

If you’ve enjoyed this issue, don’t forget to subscribe here for weekly tips delivered straight to your inbox.

If you think this would be helpful to anyone you know, please share this newsletter and connect with me on X and LinkedIn for daily financing tips.

Have a topic you'd like me to cover? Email me at hello@lawrencefan.com.