Key Benefits of Aligning Cash Flow Cycles with Loan Repayments

Have you ever wondered how a simple adjustment in your cash flow strategy could unlock a world of benefits for your business?

Today, we're diving into a crucial (yet often overlooked) aspect of financial management for business owners - aligning cash flow cycles with loan repayments.

I’ve structured countless financing structures and witnessed how the wrong structure can hamstring a company’s cash flow. If you don’t want to be in this situation, keep reading.

In this issue, you will learn:

- Why it matters to align cash flow with loan repayment

- The impacts of a misalignment demonstrated through a case study

- Actionable takeaways

Why does the timing of cash flow matter?

As a saying goes: timing is everything.

This is true for life, business, and loan structures.

When you purchase or build an asset, you will use the asset to generate cash for your business. Different types of assets have different means of generating cash. This is broadly divided into 2 categories:

Working capital assets:

Working capital assets have a short cash flow cycle.

For a business that sells physical goods, inventory is the primary asset used to generate cash. For example, a company can purchase inventory on day 1, turn around to sell inventory at a profit, and collect cash from the sale within 60 days.

For service businesses, the employees are the cash generating asset (even though they are technically not assets on the balance sheet). For example, while employees are paid biweekly, they can complete projects and generate cash in as little as a week.

The lesson here is to understand that working capital assets should have a fast pace of cash generation.

To learn more about working capital and the cash conversion cycle, read this.

Fixed assets:

Fixed assets have longer cash flow cycles.

Fixed assets are assets like real estate, leasehold improvements, manufacturing equipment, delivery trucks, and etc. These assets all have a useful life over one year. The company uses fixed assets to support the primary operation and are indirectly involved in helping the company generate cash. For example, manufacturing equipment is used to produce the inventory for sale, delivery trucks are used to ship finished goods to customers, renovations improve the aesthetics of the retail store, and etc.).

Intangible assets such as intellectual property (IP), copyrights, or trademarks can also generate cash for the business.

When financing gets involved:

When financing is used to acquire these assets, the loan needs to be repaid. There are two common types of loans:

Line of Credits (”LOC”)

A line of credit can be drawn down, repaid, and redrawn at any time. This is most commonly used to finance working capital assets.

When inventory is purchased, the LOC advances cash to the company to pay the invoice. When the inventory is sold, cash is generated and is used to repay the LOC. This cycle repeats over and over again.

Term Loans

Term loans are initially drawn down as a lump sum and repaid through instalments over time. Term loans are most commonly used to finance fixed assets with the repayment term (also known as amortization) lined up with the useful life of the asset.

For example, a delivery truck can be used to support the company’s sales over its useful life of 7 years. A portion of the cash generated through sales will be used to repay loan instalments over 7 years.

The key here is that the loan is repaid over the useful life of the asset, regardless of how long its life is.

Now, what happens when the timing of cash flow and loan repayments are misaligned?

Case study: The Impacts of Misaligned Cash Flows with Loan Repayment

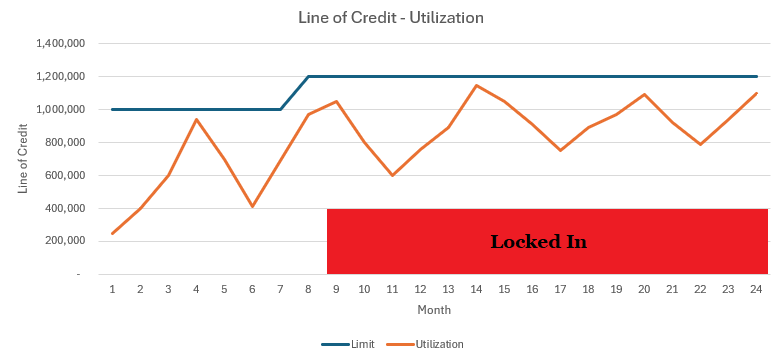

Company A has a $1,000,000 line of credit with utilization rates following its working capital cycle. The company has suffered losses and needs additional $200,000 in liquidity to purchase inventory. To support the increase, the owner used a property and pledged it as collateral to the bank. In the following months, business performance has improved but continued to operate at break even profitability. The following chart outlines Company A’s utilization against its LOC:

From this chart, the LOC increase was granted in month 8. The company instantly increased their utilization beyond the original limit of $1,000,000 to buy inventory. In the following months, the company operated at break even and utilization never reduces under $400,000 again.

This creates a “locked in” portion of the line of credit (the red box). The locked in portion is the permanent amount within the LOC that does not revolve. In other words, the company’s regular working capital cycle is not capable of reducing the LOC under $400,000.

In this scenario, the timing and value of assets financed are no longer aligned with the structure of the loan. This creates several problems:

- No repayment structure

- There is no formal repayment structure since the loan is made under a LOC - there is no mandatory obligation to make principal repayments. The LOC can be repaid if there is cash but in this case, there isn’t enough cash flow to reduce the locked in portion.

- Higher interest costs

- Since the locked in portion is stagnant, utilization on the LOC remains elevated. This directly leads to higher interest costs.

- The locked-in portion will hamstring the LOC, limiting flexibility and access to cash.

- The LOC is intended to give the company quick access to cash as its utilization revolves between peaks and troughs. However, the stagnant locked-in portion of the LOC reduces significant access to the line of credit. In the event of an economic downturn or business disruption, access to cash will no longer be available.

- Impact on financial covenants (current ratio)

- Utilization under the LOC is categorized within the company’s current liabilities. The current assets (inventory) has remained within its regular operating levels. Note that the Current Ratio is a standard financial covenant for LOCs and is calculated as: Current Ratio = Current Assets / Current Liabilities.

- Since the utilization of the LOC has increased, current liabilities will also increase. This reduces Company A’s current ratio and can put the company in breach of its financial covenant with the lender. This will be seen as a red flag to the bank, which raises the company’s credit risk profile.

The Solution:

The problem stems from the locked in portion of the LOC and the absence of a repayment structure. So naturally, the solution is to “term out” the line of credit by converting the locked in amount into a term loan.

Terming out the line of credit will solve all of the problems above.

- Repaying the loan in monthly instalments will reduce the debt outstanding over time.

- Interest cost will reduce in line with the reduced loan balance.

- Removing the locked-in portion releases the capacity on the LOC, providing flexibility and access to cash.

- From an accounting perspective, the term loan is separated into a current portion and long-term portion on the balance sheet. This reallocates a significant portion current liabilities into long-term liabilities, which will instantly improve the current ratio metric.

The biggest consideration to make is the amortization of the term loan. Since the company is now operating at break even, it likely wont have excess cash to make large monthly instalments. By setting a longer amortization, loan repayments are minimized, which provides more operating flexibility for the company while reducing total debt.

Actionable Takeaways:

Following the lessons learned from the case study, every company needs to take these actionable steps:

- Evaluate Your Cash Flow: Assess the timing of your cash inflows against loan repayments.

- Consider Restructuring: In the event of a misalignment, consider the benefits of restructuring credit facilities for optimal alignment.

- Implement Controls: Make sure controls are in place to ensure:

- Cash flow received from sale of current assets line up with the repayment of current liabilities.

- All fixed assets are financed through term loans over the useful life of the asset or shorter (never longer).

- All current assets (inventory) are financed through a line of credit. Never use a term loan to finance short-term needs.

- Sufficient cash buffer within the line of credit to cover at least 2 months of operating expense to hedge against any business disruptions.

Following these steps will ultimately improve the financial stability of the company and enhance business resilience. By simply aligning cash flow with loan repayments, this ensures a smoother financial journey, lowers interest cost, and reduces credit risk.

That's it for this week. Thank you for reading Financing Journey. See you next Saturday.

If you’ve enjoyed this issue, don’t forget to subscribe here for weekly tips delivered straight to your inbox.

If you think this would be helpful to anyone you know, please share this newsletter and connect with me on X and LinkedIn for daily financing tips.

Have a topic you'd like me to cover? Email me at hello@lawrencefan.com.