How to Influence Your Loan Pricing

Before signing up for a loan with the bank, the bank will provide a term sheet outlining all the key terms and conditions of the loan.

The first thing business owners look for is the pricing. You skim through the term sheet until you find the line “Interest Rate”.

It reads “Prime + 4.00%”. Your heart drops and the first thought is: Why is the loan so expensive?

When it comes to pricing a loan, most owners don’t know how banks come up with their pricing. In this issue, I’m going to demystify this topic once and for all.

Let’s dive in.

In this issue, you will learn:

- The bank’s pricing benchmark

- Factors affecting loan pricing

- The bank’s decision making process

- How to influence pricing decisions

The Bank’s Pricing Benchmark

To understand how the bank prices a loan, we must first understand their pricing benchmark.

Banks are in the business of making money and the most common measurements of profitability are return on equity and return on invested capital. While different banks use different metrics, there are two key factors to know: “Return” and “Capital”.

Return is measured by the size of its profits. This is simply the net income earned from the credit facilities. The bigger the net income, the better the return.

Capital is a complicated topic but I’ll explain it in the simplest way possible. Before the bank can lend out money, it needs to first get that money (the capital). Capital comes from attracting cash deposits from customers or by borrowing money from other banks. Once the bank has enough capital, the bank is required to hold a minimum amount of capital for each loan. Banks need to set aside capital because if the loan goes into default, the bank is on the hook to pay back the deposit to its customers.

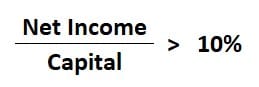

The goal of the bank is to maximize its returns. Let’s assume banks have a Return on Capital target of 10%. This can be seen as:

Now that we have the 2 key factors, let’s look into the drivers of these factors.

Drivers of Net Income

Before the bank can price a loan, it needs to know how much income it can earn throughout the life of the loan. Since the decision is being made before a loan is issued, banks estimate the income on a forward looking basis. Sources of income include:

- Loan interest: The interest you pay over the life of the loan. Banks assess the company’s forecast and needs to determine the average utilization of the loan. The utilization is then multiplied by the interest rate to arrive at the interest to be received.

- Deposits: When customers of the bank deposit cash into their bank accounts, banks can use this money and lend it to others to earn interest income. To compensate the depositor, banks pay interest on the deposit. Typically, the interest rates charged on loans is higher than the deposit interest paid. This difference in rate is what the bank earns by holding deposits and a portion of income is factored into the pricing of your loan.

- Cash management fees: These are the transactional fees you pay for using the bank’s services (i.e. internet banking, cheque, EFT, ACH, wire payments, and etc.).

- Foreign exchange fees: When you convert cash from one currency to another (i.e. CAD to USD), the bank takes a spread on the transaction (~2.5%). This spread is recognized as the FX income.

- Other fees: Business loans are usually structured with additional fees such as a set-up fee, monthly loan administration fees and standby fees.

I know what you are thinking… that’s a lot of fees. I don’t disagree but hear me out. When you have a need for banking services, these fees are unavoidable. Treat it as a cost of doing business.

Drivers of Capital

The determinants of capital is a bit of a black box so I won’t bore you with the regulatory background. But you should know these drivers of capital:

- Risk rating: The most important driver of capital requirements is the risk rating of the company. If a company is determined to be ‘high risk’, the bank needs to set aside more capital. High risk companies have a higher probability of default so to balance this risk, more capital is needed to minimize the bank’s risk to repay deposits back to the holder.

- Security: Loans are secured by collateral. If a company has a lot of collateral supporting the loan, less capital is required to be held. This is because banks will liquidate the collateral when the loan is in default and use the sales proceeds to pay off the loan and minimize its losses. When a loan is well secured with valuable collateral, the likelihood of having the loan fully repaid is higher, which means there is less risk. To learn more about collateral, read this.

- Size of the loan: The larger the loan, the more money is at stake, which means more capital is required.

- Term of the loan: The longer the term of the loan, the longer the risk exposure there is for the bank, which means more capital is required.

Let’s move on to the fun part…

Pricing Time

Since banks use the Return on Capital benchmark to determine its pricing, the decision becomes a game of math.

In the hypothetical example, when the loan generates returns greater than 10%, the deal gets the bank’s pricing approval. However, if return is less than 10%, banks have limited levers to improve returns. The easiest and most straightforward method is to increase the interest rate and fees.

Keep in mind that the bank must also be aware that it cannot simply set interest rates abnormally high since it needs to compete against other banks pitching for your business. (Hint: always ask multiple banks to pitch for your business to keep their bids honest).

Here’s where you come in…

How To Influence Pricing Decisions

There are a few drivers that can be influenced by your actions:

- Consolidate banking services: If you split your banking between multiple banks, consolidate your banking with one bank. Combining the deposits, cash management, and foreign exchange transactions with one bank pools together all the fees earned, which improves the bank’s net income. This improves the numerator and improves the overall return of the loan.

- Ask for a smaller loan: If there is no immediate need for a large loan, reducing the size of the loan will reduce the amount of capital required. With the denominator reduced, this improves the overall return of the loan.

- Shorten the loan: Reducing the term of the loan reduces the associated risks, which lowers the amount of capital required.

- Bring in other bidders: With multiple banks bidding to win your business, some banks may opt to price a loan under their hurdle requirements. The bank is making a long-term strategic play to win over the full banking relationship with hopes of further business growth, leading to more banking opportunities.

- Renegotiate based on financial improvements: When the business grows and its financial performance improves, this may improve the company’s overall risk rating. Since this is the biggest driver of capital requirement, a lower risk rating allows the bank to hold less capital. In order for the bank to remain competitive against other banks, it will be forced to reduce its pricing.

Now that you understand the pricing framework used by banks, you can use the tips above to influence their decision. Take some time to reevaluate your company’s financial position and the pricing of its loan to see if you are being priced fairly in the market.

That's it for this week. Thank you for reading Financing Journey. See you next Saturday.

If you’ve enjoyed this issue, don’t forget to subscribe here for weekly tips delivered straight to your inbox.

If you think this would be helpful to anyone you know, please share this newsletter and connect with me on X and LinkedIn for daily financing tips.

Have a topic you'd like me to cover? Email me at hello@lawrencefan.com.